“I would not look to the U.S. Constitution, if I were drafting a Constitution…I might look at the Constitution of South Africa. That was a deliberate attempt to have a fundamental instrument of government that embraced basic human rights, and had an independent judiciary… It really is, I think, a great piece of work.’’ – Former U.S. Supreme Court Justice Ruth Bader Ginsburg.

One key aspect of our constitution is that it provided our judicial branch of government a steadfast means which they used to protect our democracy when both the legislative (parliament) and executive (president) branches failed to curtail corruption.

With today’s budget speech taking place, South Africans will be focussed on any announcement relating to the tax-payer carrying the increasing burden of poorly run State Owned Entities (SOEs). Few, however, have noticed the recent increased pressure from the Finance Minister on government pensioners to shoulder this burden.

Recently, the Public Investment Corporation (PIC), which manages the Government Employees Pension Fund (GEPF), came under pressure from Finance Minister Malusi Gigaba to provide Eskom with a R5bn short-term loan which they viewed as “bridging finance”. The loan was extended at a slightly higher interest rate than the market rate (JIBAR). However, the PIC could have potentially invested that same capital elsewhere earning a higher return with lower risk. This loan effectively means that government pensioners had to bail out a near defaulting SOE. With private sector funding being expensive (due to the credit rating downgrades) and an estimated R1.6 trillion of assets in the GEPF, it may have seemed like an extremely attractive and cheap borrowing source.

The loan was heavily criticized, especially by labour unions and media, and rightly so. The performance of the SOEs have been woeful of late, making poor capital allocation decisions and being plagued by corruption. If this track-record is anything to go by, a loan to an SOE is not necessarily the best investment decision, especially for aging pensioners who can ill afford to have poor investment decisions taken on their behalf. However, without this loan having been extended to Eskom, our largest SOE may well have faced near collapse with significant knock-on effects to the broader economy.

With a strong constitution, a renewed executive branch and soon to be renewed legislative branch supporting it, we are hopeful that the GEPF will be protected from looting and the SOEs encouraged to become self-funding by all branches of government, instead of relying on government pensioners to bail them out.

Things seem to be moving in the right direction; last week for example, Transnet announced its plans to boost its revenues by more than half to R100 billion by expanding into other African countries and President Cyril Ramaphosa announced his intention to root out SOE corruption in his State of the Nation Address.

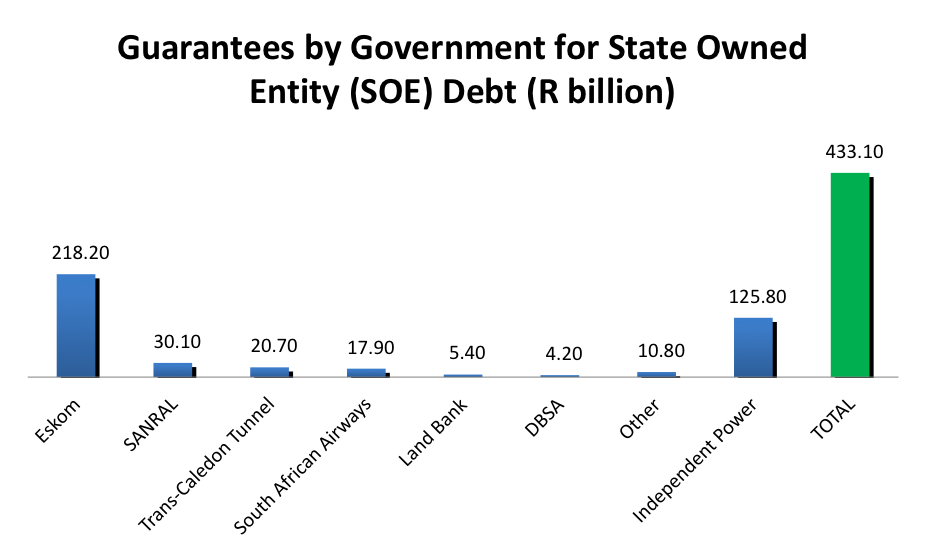

With the budget speech taking place today, it is imperative that Minister Gigaba does not continue to ask government pensioners to help fund the shortfall in SOEs. Currently, South Africa’s debt to Gross Domestic Product (GDP) ratio stands at 52%. With South Africa spending more on interest servicing costs (refer to our previous article) than tertiary education, and Eskom’s debt adding another 12% to the debt to GDP ratio, South Africa can ill afford to continue borrowing at near unaffordable interest rates. Forcing government pensioners to help fund weak SOEs is not the solution. Rather, avenues that lead to aggressive and prudent cuts to public sector spending (especially the wage bill) need to be emphasized.

Graph data: Helen Suzman Foundation.