Myopia – or more commonly known as short-sightedness – has been the cause of many people’s frustration. Sixty years ago, 10-20% of the Chinese population was short-sighted. Today, up to 90% of Chinese teenagers and young adults are. In Seoul, South Korea 96% of 19-year-old men are short-sighted. By 2020, it is estimated that up to one-third of the world’s population could be affected by short-sightedness. Clearly, short sightedness is on the rise. The question is why?

Seeing the forest from the trees

The highly regarded Nature Journal of Science relatively recently published studies providing evidence that short-sightedness is partly caused by spending too much time reading, studying or focussing on computer and smartphone screens. Those children that spent more time playing outside and less time inside doing homework had a lower prevalence for developing short-sightedness. There are different theories as to why spending more time outside lowers the risk. It is postured that on a biological level, ‘’sustained close work could alter the growth of the eyeball as it tries to accommodate the incoming light and focus close-up images squarely on the retina.’’ Greater viewing distances outside, along with increased light exposure could decrease the progression of short-sightedness.

Those hard studying students are not the only ones struggling with the condition. The market tends to focus on the short-term, seeing what is directly in front of them, extrapolating the present into the future and ignoring the longer term potential, which may be completely different to the present. Currently, the market is focussed on investing in U.S. tech companies at any price and ignoring blatantly cheap companies in unattractive sectors like oil & gas and shipping. Take the performance of various value-based managers (value investing: buying companies at prices less than what they’re worth) over the recent past (one month and 12 months):

| “Value’’ Manager | 1 Month US$ Performance to end August 2019 | 1 Year US$ Performance to end August 2019 |

| Contrarius Global Equity Fund | -12.9% | -32.9% |

| Dodge & Cox Global Stock Fund | – 3.6% | -14.8% |

| Conventum Lyrical Fund | – 8.6% | -12.5% |

| Orbis Global Equity Fund | – 1.9% | -10.4% |

| Tweedy Browne Global Value Fund | – 1.8% | – 8.1% |

| Mundane World Leaders Fund | – 4.5% | 0.1% |

| MSCI All Countries World Index | – 3.7% | – 2.4% |

Performance to end August 2019 and in US$, net of all fund manager fees.

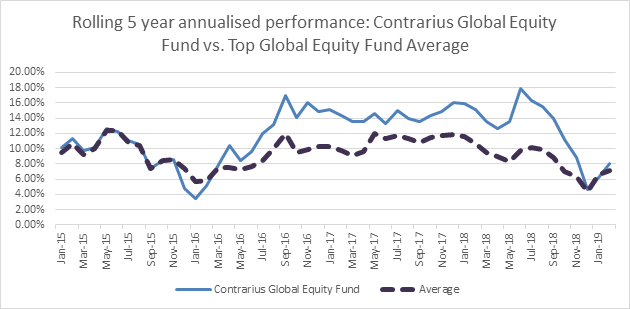

Clearly, the prior one month and 12-month performance of most of the more well-known value managers has been poor. Now take a step back and look at the longer-term. Take the rolling five year annualised performance of a recent poor performer like the Contrarius Global Equity Fund (in blue below) and compare that to the average performance of the top quartile global equity funds (in purple below). Clearly, a good quality value fund, like the Contrarius Global Equity Fund, tends to outperform the average top global equity fund over most rolling five year performance measurement periods, despite materially underperforming over many shorter performance measurement periods:

The average rolling five-year annualised return for the Contrarius Global Equity Fund since 2015 has been 11.3%, net of fund manager costs. Since month-end, the Contrarius Global Equity Fund is up again 9.3%, illustrating how volatile short-term performance can be. These funds are managed to deliver good performance over full investment cycles, typically lasting five years. Similar to delaying the progression of myopia, those investors who are willing to look past the close-up performance and keep their eyes focussed on the longer-term performance horizon, tend to achieve the best outcome.

The Nature Journal article is available at: https://www.nature.com/news/the-myopia-boom-1.17120

As always, we welcome any questions, queries or comments you may have.