Robinhood is a fintech company that has become extremely popular with younger stock traders, in particular millennials. Their app allows you to trade stocks for ‘’free’’ i.e with no commission being levied on the buying or selling of shares. The company is valued at $7.6 billion. Clearly, Robinhood has to make money somehow in order to justify the valuation.

Their stated revenue model is to collect interest on cash and securities in Robinhood client accounts, similar to how a bank collects interest on cash and deposits. This is a volume game. The more clients they have, the more cash there should be in client accounts and the more interest revenue they can earn. However, millennials trading notional amounts of stocks doesn’t support a valuation of $7.6 billion. Generally, most younger clients probably don’t have significant excess cash sitting in their trading accounts for Robinhood to earn interest on.

Contrary to their stated revenue model, Robinhood actually makes most of their money on a practice called ‘’order routing’’, which is a hidden cost to the investor.

What is order routing?

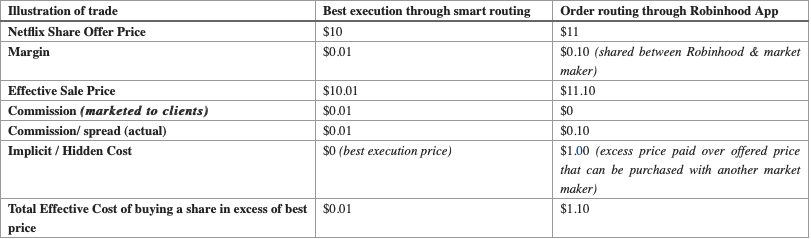

Order routing is a practice where an order (buying or selling a share, for example) is directed or ‘’routed’’ to a market maker. Market makers pay Robinhood for these orders to be directed to them. In the case of Robinhood, the market makers are Two Sigma, Citadel, Apex and KCG. In practice, it works something like this: if you want to buy a share of a company, like Netflix, using the Robinhood app, the app directs this purchase instruction to one of their market makers like Citadel. Citadel then adds a margin, called a ‘spread’ on the price that a seller is willing to sell his Netflix share at. Citadel then shares this spread with Robinhood, in an undisclosed proportion.

The problem with this practice is that another market maker outside of their order routing agreement might have a seller willing to sell her Netflix shares at a lower price than what is available at Citadel. Citadel knows there is a buyer for the Netflix share, due to their agreement with Robinhood. It, therefore, doesn’t matter if the Netflix share they can offer to the Robinhood buyer is offered at a higher price than what another market maker is willing to offer the share at. By purchasing the share at a higher price than what he can elsewhere, the Robinhood investor is being disadvantaged. This is a hidden cost that the buyer is not aware of.

Here is the crux of the matter, there is no such thing as a free lunch. If the product is being marketed as ‘’free’’, most likely you’re the product. In this case, it is like playing poker with the face of your cards facing your opponents.

In summary, a comparative trade might look as follows:

By some estimates, the ‘spread’ Robinhood charges is on average 50x that which smart router brokers charge without these market making agreements. Unlike Robinhood, which has order routing agreements with four market makers, the best brokerage systems search for the best stock price available at the time of the client’s purchase / sale order. This is called “smart routing”, and it allows the client to get the best execution price possible, regardless of which market marker offers it.

Recently, major stockbroking firm Charles Schwab announced it will be following Robinhood’s lead and also reduce its brokerage fees to $0. Most likely, their clients, like the Robinhood clients, will be paying indirectly through order routing agreements to help make up the revenue shortfall.

There are many other types of purported ‘’low cost’’, “negative fee” or “free” investment products, like passive exchange traded funds (ETFs), that are much higher cost than what investors realise. Investors should conduct a full due diligence on both the implicit (hidden) as well as explicit charges associated with these products. Our article dealing with the total costs involved with various marketed ‘’low cost’’ products is available on our website: When in Doubt, Just ETF It! https://fintaxgroup.com/doubt-just-etf/

As always, we welcome any comments, queries or questions you may have.